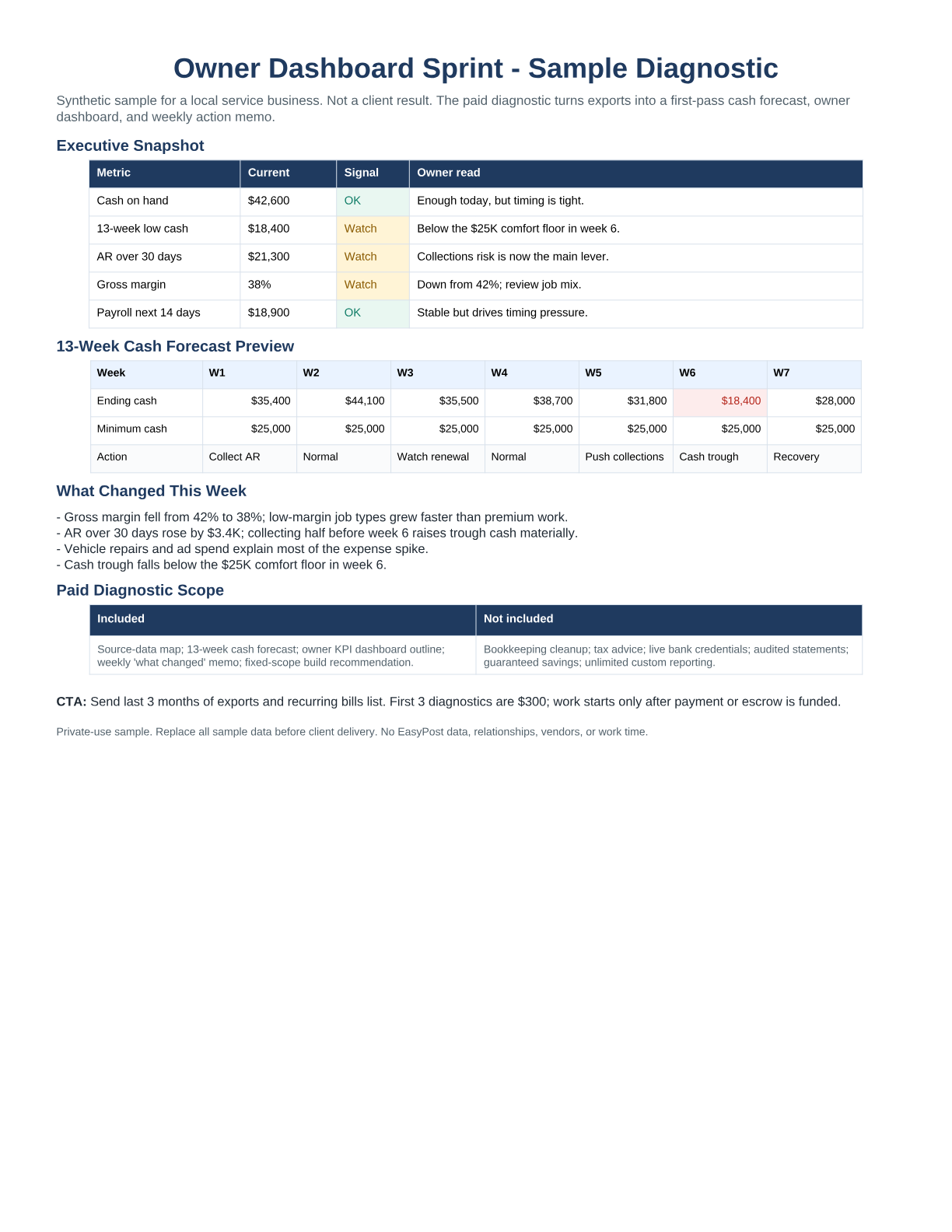

Owner cash sprint

HVAC / contractor / local service

Can we make payroll, buy parts, and still keep enough cash cushion?

Built from QuickBooks exports, bank CSV, open invoices, recurring bills, and payroll timing.

The output is a 13-week cash floor and the few calls the owner should make first.

$22Kprojected low cash week

1.8xpayroll coverage at low point

$41KAR over 30 days

| Week | Pressure point | Owner action |

|---|

| 3 | parts orders hit before deposits | delay noncritical truck stock |

| 7 | cash floor after payroll | collect two overdue commercial invoices |

| 11 | install margin dip | review labor hours by job type |

SBA buyer model

broker / acquisition buyer

Does the deal still work after debt service, rent, and a realistic stress case?

Built from listing financials, seller-disclosed SDE, rent, lease terms, down payment, and loan

assumptions. It gives the buyer a clean first-pass view before asking for deeper diligence.

20%down payment case

1.31xbase DSCR estimate

0.96xstress case DSCR

- Normalize owner benefit against payroll, rent, add-backs, and working capital.

- Separate seller-financing, SBA, and cash-buyer assumptions.

- List the diligence questions that decide whether an LOI is worth writing.

CPA referral packet

bookkeeper / advisor overflow

Can the client see cash, AR, AP, and margin without turning the CPA into a dashboard shop?

Built as an export-only support layer for clients who already have bookkeeping help but need a

decision packet. It keeps tax, cleanup, and advisory boundaries clear.

6exports mapped

4source-data gaps flagged

2 pageshandoff summary

- Map source exports to the owner-facing dashboard fields.

- Flag missing customer, job, or class coding before deeper reporting work.

- Give the CPA/bookkeeper a clean "what changed and why" client summary.

Lender-ready view

borrower / referral partner

Is the borrower prepared enough to talk about cash flow without hand-waving?

Built for an owner heading into an SBA, equipment, or working-capital conversation. It packages

cash timing, debt load, and documentation gaps before a lender has to chase them.

$18Kmonthly debt service tested

9documents requested

3underwriting gaps

- Convert exports into a borrower cash-flow story with assumptions visible.

- Show base, tight, and downside cash cases without promising approval.

- Give the owner a document checklist before the lender conversation.

Figures above are synthetic examples. Real diagnostics use client-provided exports only and do not require live bank credentials.